You started your business because you’re great at what you do—whether that’s building decks, designing websites, or providing healthcare services. But somewhere between landing clients and delivering excellent work, there’s this whole other job waiting for you:

The Books.

If you’re wondering whether the importance of bookkeeping is really worth the hassle, here’s the short answer: absolutely. Clean books aren’t just about staying out of trouble with the IRS. They’re the difference between guessing and knowing, between scrambling and planning, and between surviving and thriving.

Let’s break down exactly why keeping good books matters for your small business and how to actually make it happen.

Key Takeaways From This Article

- Clean books replace guesswork with real financial clarity.

- Accurate records help you manage cash flow and avoid payroll or vendor surprises.

- Proper categorization maximizes tax deductions and reduces audit risk.

- Up-to-date financials improve your chances of getting loans or financing.

- Monthly reconciliations catch errors, duplicate charges, and potential fraud.

- Tracking profitability shows which services actually make you money.

- Consistent bookkeeping prevents year-end panic and expensive cleanup.

What “Good Books” Actually Mean

Before we dive into the why, let’s clear up the what. When accountants and bookkeepers talk about “clean books,” we’re not talking about fancy spreadsheets or complicated software. We mean financial records that are:

- Timely: Transactions recorded within days, not months

- Accurate: Numbers that actually match your bank statements

- Categorized correctly: Business expenses properly separated and classified

- Reconciled regularly: Your software matches your actual bank and credit card balances

- Separated: Business and personal finances kept completely apart

- Documented: Receipts and invoices backed up and organized

Think of it like keeping your workspace organized. You could technically work in chaos, but you’d waste hours looking for tools, make mistakes, and probably miss opportunities.

Here’s what the difference looks like in practice:

Clean vs. Messy Books

| Aspect | Clean Books | Messy Books |

| Bank Reconciliation | Monthly, all transactions match | Hasn’t been done in 6+ months, mystery charges everywhere |

| Expense Categorization | Office supplies in “Office Expense,” client meals in “Meals & Entertainment” | Everything dumped into “Miscellaneous” or “General Expense” |

| Personal vs. Business | Separate accounts, clear boundaries | Personal groceries mixed with business supplies, family dinner on the business card |

| Receipt Documentation | Digital copies stored and linked to transactions | Shoebox of faded receipts, many missing entirely |

| Monthly Close | Books closed within 2 weeks of month-end | No regular review, financials always “in progress” |

| Tax Readiness | Clean reports ready at any time | Panic and scramble every April |

Example: Sarah runs a local landscaping company. For her first two years, she threw receipts in a drawer and updated QuickBooks “whenever she had time”—which turned out to be never. When tax season hit, her accountant spent eight billable hours trying to reconstruct her income and expenses. The bill was $1,200, and Sarah still missed deductions worth about $3,500 because the records were too messy to defend.

After implementing proper bookkeeping best practices with weekly entry updates and monthly reconciliations, Sarah’s tax prep took two hours. Her accountant found legitimate deductions she’d been missing, and Sarah actually got a refund.

Better Decisions Start With Better Data

Here’s where the importance of bookkeeping moves from “avoiding problems” to “growing your business.” You can’t make smart decisions with bad information.

Cash Flow Visibility

Cash flow management is the lifeblood of any small business. You might have $50,000 in outstanding invoices, but if your bank account shows $2,000 and payroll is due Friday, those invoices won’t help you.

Reconciled books show you:

- How much cash you actually have right now

- Your cash burn rate (how fast you’re spending)

- When large payments are coming in or going out

- Whether you can afford that new hire or equipment purchase

Example: Mike owns a small construction company. He looked at his profit and loss statement and saw he’d made $18,000 last month—great news! But when he checked his actual cash position, he had only $4,200 in the bank. Why? Because $22,000 of that income was still sitting in accounts receivable, and he had $6,500 in bills due within two weeks.

Without proper cash flow tracking, Mike might have committed to a new project that required upfront material purchases, putting his business in a dangerous cash crunch. His reconciled books helped him see he needed to either collect on those outstanding invoices or wait before expanding.

12-Month Cash Flow Example

| Month | Cash In | Cash Out | Net Flow | Bank Balance |

| Jan | $28,500 | $24,200 | +$4,300 | $12,400 |

| Feb | $31,200 | $26,800 | +$4,400 | $16,800 |

| Mar | $18,900 | $29,100 | -$10,200 | $6,600 |

| Apr | $42,100 | $27,500 | +$14,600 | $21,200 |

| May | $35,800 | $31,200 | +$4,600 | $25,800 |

| Jun | $29,400 | $28,900 | +$500 | $26,300 |

Notice March? That negative cash flow month could have been a crisis if Mike hadn’t been tracking his patterns. Because he reviewed his financials monthly, he knew March was typically slow and planned accordingly.

Profitability & Pricing

Not all revenue is created equal. You might be busy all the time but still not making money if you’re pricing jobs wrong or focusing on the wrong services.

Job costing and tracking gross margin by product or service line shows you which parts of your business actually make money—and which ones are costing you.

Example: Jennifer runs a marketing agency offering social media management, graphic design, and website development. She was working 60-hour weeks and bringing in decent revenue, but somehow never had much left over.

When she started tracking her financials properly and analyzed gross margin by service, she discovered:

- Social media management: 65% gross margin (highly profitable)

- Graphic design: 52% gross margin (solid)

- Website development: 18% gross margin (barely breaking even)

The website projects took forever, required expensive subcontractors, and had too much “scope creep”. Armed with this data from her financial statements basics, Jennifer raised her website prices by 40% and focused her marketing on social media services. Within six months, she was working 45-hour weeks and earning 30% more profit.

Gross Margin by Service Example

| Service | Revenue | Direct Costs | Gross Margin | Margin % |

| Social Media Mgmt | $45,000 | $15,750 | $29,250 | 65% |

| Graphic Design | $28,000 | $13,440 | $14,560 | 52% |

| Website Development | $32,000 | $26,240 | $5,760 | 18% |

| Consulting | $18,000 | $4,500 | $13,500 | 75% |

This is the kind of insight you can only get from accurate expense tracking tips and proper categorization in your bookkeeping system.

Tax Compliance Without the Drama

Let’s be honest—nobody starts a business because they love dealing with taxes. But the importance of bookkeeping for tax purposes can’t be overstated. Clean books are the difference between maximizing your deductions and leaving money on the table (or worse, facing an audit you’re not prepared for).

Deductions & Credits

The IRS lets small businesses deduct legitimate business expenses—but you have to prove them. That means proper categorization, documentation, and an audit trail documentation that shows what you spent, when, and why.

Example: Tom runs a consulting business from his home office. With messy books, he claimed a basic home office deduction of about $1,500. After cleaning up his books and working with a bookkeeper who understood tax deductions for small business, he was able to legitimately document:

- Home office deduction (actual expense method): $3,200

- Vehicle expenses (business mileage): $4,100

- Professional development and courses: $2,800

- Business meals with clients: $1,900

- Software and subscriptions: $1,400

The difference? An additional $10,900 in deductions, saving him roughly $3,270 in federal taxes alone—all from expenses he was already incurring but not properly tracking.

Clean categorization in your chart of accounts setup means:

- Office supplies don’t get mixed with inventory

- Business meals are separated from entertainment (different rules)

- Vehicle expenses have mileage logs attached

- Equipment purchases are properly capitalized vs. expensed

Audit-Ready Records

Here’s a statistic that keeps business owners up at night: small businesses have a higher audit risk than larger corporations. But here’s the thing—an audit is far less scary when your books are clean.

Audit-ready records mean:

- Every transaction has a matching receipt or invoice

- Bank statements reconcile perfectly to your bookkeeping software

- Mileage logs are contemporaneous (recorded when trips happen, not reconstructed later)

- Large or unusual expenses have notes explaining the business purpose

- Revenue and expenses are categorized consistently

Example: Angela’s home staging business got selected for an IRS audit. Because she’d been using outsourced bookkeeping services and maintained excellent records, the audit took only one meeting. Her bookkeeper provided:

- Reconciled bank statements showing every transaction matched her books

- Digital receipt files organized by month

- A detailed mileage log showing client addresses and purposes

- Clear notes on any large purchases

Result? No adjustments, no penalties, no drama. Compare that to her friend who faced a similar audit with messy books and ended up with $8,500 in additional taxes and penalties because he couldn’t substantiate his deductions.

Tax Deadlines & Documents Checklist

| Entity Type | Key Deadlines | Essential Documents Needed |

| Sole Proprietor | April 15 (Schedule C with Form 1040) | Profit & Loss Statement, mileage logs, Form 1099-NEC for contractors paid $600+ |

| Partnership | March 15 (Form 1065) | Balance sheet, profit and loss statement, partner K-1s, receipts for partnership expenses |

| LLC (Single-Member) | April 15 (Schedule C) | Same as sole proprietor—LLC doesn’t change tax treatment unless you elect otherwise |

| S-Corp | March 15 (Form 1120-S) | Balance sheet, P&L, payroll records, shareholder distributions, reasonable compensation documentation |

| C-Corp | April 15 (Form 1120) | Complete financial statements, depreciation schedules, shareholder meeting minutes, dividend records |

If you’re running payroll, add quarterly Form 941 filings and annual W-2/W-3 preparation to your calendar. Missing payroll tax deadlines results in penalties that add up fast.

Fuel for Financing and Growth

Whether you’re looking to buy equipment, hire employees, or expand locations, you’ll likely need outside financing at some point. And lenders or investors have one question: “Show me your financials.”

Lender/Investor Confidence

Banks and investors aren’t interested in your gut feeling about how well the business is doing. They want to see actual numbers—and they want those numbers to be reliable.

Up-to-date financial statements (profit and loss statement, balance sheet for beginners, and cash flow forecast) tell the story of your business in a language lenders understand.

Example: David wanted to buy a food truck to expand his catering business. He approached his bank for a $75,000 loan. The loan officer asked for:

- Two years of profit and loss statements

- Current balance sheet

- Cash flow projections for the next 12 months

David had been keeping clean books with monthly reconciliations. He provided everything within 48 hours. The bank approved his loan in two weeks at a competitive interest rate.

His competitor, who applied around the same time with messy books, spent six weeks trying to reconstruct financials. When he finally submitted them, the numbers were inconsistent and raised red flags. His loan was denied.

Clean books from proper small business accounting don’t just get you approved—they get you better terms.

Planning & Forecasting

You can’t plan for the future if you don’t know where you’ve been. Reliable historical data makes your forecasts realistic and helps you make smart decisions about when to hire, when to expand, and when to pull back.

Example: Rachel owns a retail shop with two years of clean financial data. When reviewing her financial KPIs for SMEs, she noticed:

- December revenue was typically 3x her monthly average

- January and February were consistently slow (60% of average)

- Labor costs in Q4 were eating up profits because she was hiring too late

Armed with this insight, she:

- Built up cash reserves before the slow season

- Hired seasonal help in early November instead of mid-December

- Negotiated extended payment terms with suppliers for January orders

Her forecast vs. actual revenue tracking showed she hit her projections within 5%—giving her the confidence to sign a lease on a second location.

Forecast vs. Actual Revenue Example

| Month | Forecast Revenue | Actual Revenue | Variance | Notes |

| Jan | $28,000 | $26,400 | -$1,600 | Slower than expected post-holiday |

| Feb | $30,000 | $32,100 | +$2,100 | Valentine’s promo outperformed |

| Mar | $35,000 | $34,200 | -$800 | On track |

| Apr | $38,000 | $41,500 | +$3,500 | Spring surge started early |

Regular variance analysis helps you adjust your strategy and get better at predicting the future.

Operational Efficiency & Risk Control

Beyond taxes and financing, good bookkeeping powers your day-to-day operations and protects you from costly mistakes and fraud.

AR/AP Discipline

Accounts receivable management and your accounts payable process might sound like boring accounting jargon, but they directly impact your cash and vendor relationships.

Clean books mean:

- You invoice promptly and follow up on overdue accounts

- You pay vendors on time and catch early-payment discounts

- You avoid late fees and damaged credit relationships

- You spot customers who are consistently slow to pay

Example: Lisa runs an IT consulting firm. Before implementing proper bookkeeping, her accounts receivable was a mess. Clients often went 60-90 days without paying because she’d forget to send invoices or follow up.

After setting up a system to reconcile bank statements and track AR aging every week, she:

- Reduced her average collection time from 67 days to 32 days

- Improved cash flow by over $40,000 in working capital

- Caught two clients who’d been underpaying invoices for months

- Saved $800 annually in late fees by paying vendors on time

She also discovered she was paying the same software subscription three times—$150/month for nearly a year—because she wasn’t reviewing her expenses regularly.

Fraud & Error Prevention

Small business fraud is more common than you’d think—and it’s often committed by trusted employees. Regular monthly close procedures and role separation help catch problems before they become disasters.

Example: Kevin owned a small manufacturing company and let his office manager handle everything: entering bills, cutting checks, reconciling accounts. He trusted her completely.

After three years, Kevin finally reviewed his books carefully and found something odd. His “office supplies” expense was running $3,500/month—for a 12-person company. When he dug deeper, he discovered his office manager had been writing checks to herself and coding them as office supplies. Over three years, she’d stolen $108,000.

If Kevin had implemented basic fraud prevention controls—like reviewing reconciliations monthly, requiring dual signatures on large checks, or having someone else open the bank statements—he’d have caught it within weeks instead of years.

Month-End Close Checklist

| Task | Frequency | Why It Matters |

| Reconcile all bank accounts | Monthly | Catches errors, unauthorized charges, and ensures accuracy |

| Reconcile credit cards | Monthly | Prevents missed charges and fraudulent transactions |

| Review accounts receivable aging | Monthly | Identifies slow-paying customers and collection issues |

| Review accounts payable | Monthly | Ensures bills are paid on time and catches duplicate payments |

| Record depreciation | Monthly | Keeps asset values accurate for financial reporting |

| Review P&L vs. budget | Monthly | Identifies variances and informs management decisions |

| Review unusual or large transactions | Monthly | Catches errors and potential fraud |

| Close books (no more edits to period) | Monthly | Creates a reliable historical record |

Getting into a regular cadence with your monthly close checklist builds discipline and catches small problems before they become big ones.

Simple Setup That Scales

The good news? You don’t need a degree in accounting to keep good books. You just need the right tools, processes, and maybe some help.

Tools & Processes

Modern bookkeeping software for startups has made financial management accessible to everyone. But the software is only as good as how you use it.

Setting up for success:

- Choose the right software: QuickBooks Online, Xero, and FreshBooks are popular for small businesses. They connect to your bank accounts, automate data entry, and generate reports.

- Design a proper chart of accounts: This is the foundation of your bookkeeping. It’s the list of categories where every transaction gets sorted (Revenue, Cost of Goods Sold, Operating Expenses, Assets, Liabilities, Equity).

- Connect your bank feeds: Link your business checking, savings, and credit cards so transactions flow automatically into your software.

- Set a cadence:

- Weekly: Review new transactions, categorize them, save receipts

- Monthly: Reconcile accounts, review P&L, close the month

- Quarterly: Review trends, update forecasts, check in on goals

- Document your processes: Write down how you categorize common expenses, what you name vendors, and where you save receipts. Consistency makes your books cleaner.

Example: When Maria started her consulting business, she spent an afternoon setting up QuickBooks properly with help from a bookkeeper. They:

- Created a chart of accounts tailored to her industry

- Set up automatic transaction downloads from her bank

- Established rules so recurring charges (like software subscriptions) categorized automatically

- Created a simple weekly workflow: 30 minutes every Friday to review and categorize the week’s transactions

This small upfront investment saved her hours every month and kept her books current.

Want expert help getting your books set up right from the start? Check out our bookkeeping setup and training services—we’ll get you up and running with clean processes that work for your business.

Common Mistakes to Avoid

Even with the best intentions, small business owners make predictable bookkeeping mistakes. Here are the most common traps and how to avoid them.

1. Mixing Personal and Business Expenses

This is the #1 mistake we see. Using your business card for groceries or your personal account for business expenses creates a nightmare for tax deductions and makes your financial reports meaningless.

The fix: Open separate business checking and credit card accounts on day one. Even if you’re a sole proprietor, treat your business finances as completely separate.

Example: Carlos kept using his personal checking for both business and personal expenses “to keep things simple.” At tax time, his accountant had to review every single transaction—all 847 of them—to separate business from personal. The bill was $1,800. If Carlos had used separate accounts, it would have been maybe $400.

2. Skipping Reconciliations

Your QuickBooks balance means nothing if it doesn’t match your actual bank balance. Skipping monthly reconciliations means errors, bank fees, and fraudulent charges go unnoticed.

The fix: Reconcile every bank and credit card account monthly, without exception. Mark it on your calendar.

3. Misclassifying Expenses

When everything goes into “Miscellaneous Expense” or “Office Expense,” your financial reports tell you nothing, and you miss tax-planning opportunities.

Common misclassifications:

- Software subscriptions coded as “Equipment” instead of “Software/Technology”

- Client meals coded as “Entertainment” (not deductible) instead of “Meals”

- Independent contractor payments not tracked separately (you need to send them 1099s)

- Personal expenses accidentally coded as business

- Marketing costs spread across multiple vague categories

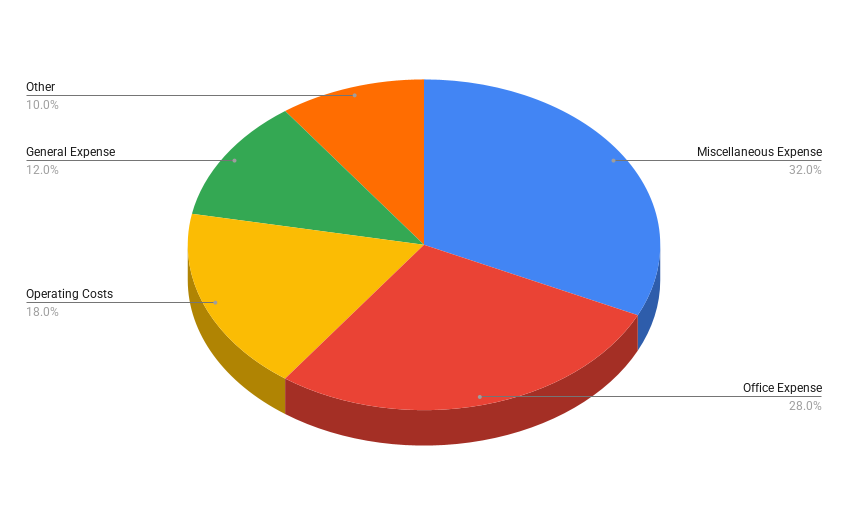

Top Expense Misclassifications for Most Small Businesses

This pie chart represents what we see when we do bookkeeping cleanup for new clients. About 90% of expenses are in vague, unhelpful categories—making financial analysis impossible.

The fix: Use specific categories consistently. If you’re not sure where something goes, mark it for review rather than guessing.

4. Ignoring Sales Tax and Payroll Compliance

Sales tax and payroll taxes are trust funds—you’re collecting money on behalf of the government. Mess these up and the penalties are severe.

The fix: If you collect sales tax, set up automatic remittance. If you have employees, use a payroll service provider that handles tax deposits and filings automatically. Don’t try to DIY this. Our payroll services handle all the compliance headaches so you don’t have to.

5. Treating Your Books as a Tax-Time Project

Trying to reconstruct a year of financials in March before your tax deadline is stressful, expensive, and error-prone.

The fix: Make bookkeeping a regular habit, not an annual event. Even 30 minutes weekly prevents year-end panic.

The Bottom Line

The importance of bookkeeping isn’t about having pretty numbers or impressing your accountant. It’s about having the information you need to run your business confidently.

Clean books help you:

- Know if you’re actually making money or just keeping busy

- Manage cash so you never scramble to make payroll

- Make smart decisions about pricing, hiring, and growth

- Maximize tax deductions and minimize IRS headaches

- Access financing when opportunity knocks

- Sleep better knowing you’re in control of your finances

Yes, bookkeeping takes time. Yes, it costs money (whether you do it yourself or hire help). But the cost of not doing it—missed opportunities, tax penalties, poor decisions, stress—is far higher.

You don’t have to be an accounting expert. You just need to commit to the basics: separate accounts, regular reconciliations, proper categorization, and monthly reviews.

And if that still feels overwhelming? That’s exactly why bookkeeping services exist. We take the headache off your plate so you can focus on what you do best—running your business.

Because at the end of the day, your books should serve you, not stress you out. Let’s make that happen.

Need help getting your books cleaned up and organized? At Bookrite Bookkeeping, we specialize in helping small business owners control of their finances. Whether you need catch-up services, ongoing bookkeeping, or just some training to get started right, we’re here to help. Contact us today to see how we can become part of your team.

Disclaimer :

The information provided in this article is for general informational and educational purposes only and should not be construed as accounting, tax, or financial advice. Every individual and business financial situation is unique, and the strategies or concepts discussed may not be appropriate for your specific circumstances. Reading this content does not establish a client relationship with Bookrite Bookkeeping. For advice tailored to your business or personal financial needs, please consult directly with a qualified accounting, tax, or financial professional.